TL;DR:

- Homeowners insurance covers HVAC damage only when caused by sudden, accidental perils listed in the policy, excluding wear and tear. California residents must also consider separate coverage for earthquakes, floods, and wildfire smoke damage, which often fall outside standard policies. Proper documentation and adding endorsements like Equipment Breakdown improve the chances of claim approval for eligible damages.

Homeowners insurance covers HVAC systems only when damage results from a sudden, accidental event listed in your policy. Standard policies exclude mechanical breakdowns, aging components, and deferred maintenance. California homeowners face an added layer of complexity: wildfires, windstorms, and earthquakes each trigger different coverage rules. Knowing exactly what your policy covers before something breaks is the difference between a paid claim and a denial. This guide explains the covered perils, common exclusions, endorsement options, and the exact steps to file a successful HVAC insurance claim in California.

Does home insurance cover HVAC damage?

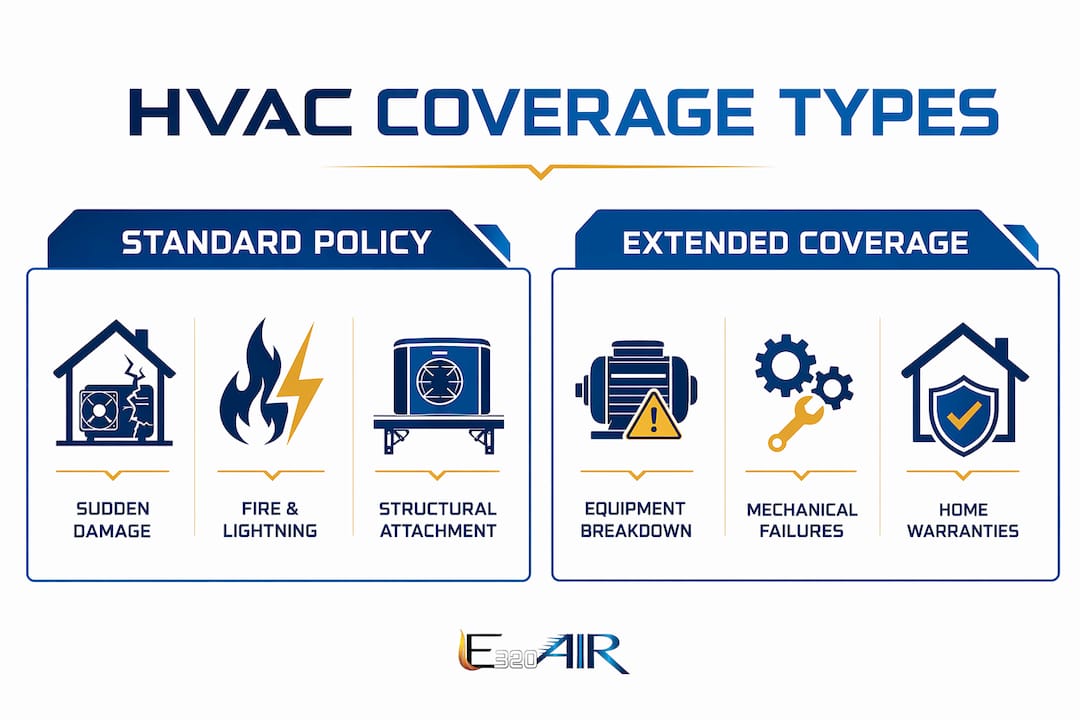

Standard homeowners insurance covers HVAC systems under Dwelling Coverage (Coverage A) when damage is caused by sudden, accidental perils named in the policy. That means a lightning strike that fries your air handler, a windstorm that crushes your outdoor condenser, or a burst pipe that floods your furnace room are all legitimate claims. What the policy does not cover is the compressor that wore out over 12 years of use, or the heat exchanger that cracked because filters were never changed.

Central HVAC units receive broader protection because they are structurally attached to the home and fall under Coverage A. Portable window units and standalone space heaters are treated as personal property, which typically means narrower named-peril coverage and lower payout limits. If you have a whole-home system, you are in a better position than someone relying on portable equipment.

The term "sudden and accidental" is the policy's gatekeeping phrase. Adjusters apply it strictly. A compressor that fails on a hot July afternoon without any external cause does not meet the threshold. A compressor destroyed when a tree branch punches through the equipment pad during a Santa Ana wind event does.

Common perils that typically trigger HVAC coverage

- Fire or smoke damage from a house fire

- Lightning strike directly damaging the unit or electrical system

- Windstorm or hail damage to outdoor condenser units

- Falling objects such as trees or debris

- Burst or frozen pipes flooding indoor air handlers or furnaces

- Vandalism or theft of outdoor HVAC components

- Vehicle impact on exterior equipment

Why wear and tear voids most HVAC claims

Insurance claims are denied when damage is attributed to wear and tear, poor maintenance, or a pre-existing condition rather than a covered peril. This is not an arbitrary rule. Insurance is designed to protect against catastrophic, unpredictable losses. It is not a maintenance contract or an appliance warranty. The distinction matters enormously when your 14-year-old air conditioner stops working in August.

Deferred maintenance is the most common reason HVAC claims fail. Dirty coils, clogged condensate drains, and neglected filters all accelerate system failure. When an adjuster sees evidence of long-term neglect alongside a claim, the denial is almost automatic. Documented pre-existing damage or deferred maintenance is often the deciding factor between approval and denial. Insurers are not obligated to pay for problems that existed before the claimed event.

Homeowners frequently mistake insurance for a home warranty, expecting it to cover any HVAC failure. That misconception leads to denied claims and surprise out-of-pocket costs. A home warranty covers mechanical breakdowns from normal use. Homeowners insurance covers damage from external, insured events. These are two completely different products solving two completely different problems.

Pro Tip: Schedule a licensed HVAC inspection every year and keep the written report on file. If you ever file a claim, that dated inspection showing a healthy system is powerful evidence that the damage was sudden, not the result of neglect.

How to extend your HVAC coverage beyond standard policies

Equipment Breakdown coverage is an endorsement you add to your existing homeowners policy. It insures mechanical or electrical failures of HVAC systems that standard policies exclude, including compressor failures, control board burnouts, and refrigerant leaks caused by internal faults. The cost is typically low relative to the potential expense of full system replacement, making it one of the most cost-effective endorsements available.

The other major variable in your policy is how it calculates your payout. ACV (Actual Cash Value) policies apply depreciation deductions, which can reduce your settlement by thousands of dollars on an older system. RCV (Replacement Cost Value) policies pay the full cost to replace the unit with a comparable new one, minus your deductible. On a 10-year-old central air system, the difference between ACV and RCV could easily exceed $3,000 to $5,000. Knowing your policy type before a loss is critical, not after. You can review California HVAC service prices to understand what replacement actually costs in your area.

Home warranties and flood insurance fill the remaining gaps. A home warranty covers mechanical breakdowns from normal use, which is exactly what standard homeowners insurance excludes. Flood insurance through the National Flood Insurance Program (NFIP) covers water damage from external flooding, which also falls outside a standard policy. For California homeowners, earthquake coverage requires a separate California Earthquake Authority (CEA) policy.

| Coverage type | What it covers | What it excludes | Typical cost |

|---|---|---|---|

| Standard homeowners (Coverage A) | Fire, lightning, windstorm, falling objects, burst pipes | Wear and tear, mechanical failure, floods, earthquakes | Included in base policy |

| Equipment Breakdown endorsement | Compressor failure, electrical burnout, control board issues | Gradual deterioration, cosmetic damage | Low add-on cost |

| Home warranty | Mechanical breakdowns from normal use | Damage from external events like storms or fire | Separate annual contract |

| Flood insurance (NFIP) | Water damage from external flooding | Internal pipe leaks, storm surge without flood declaration | Separate federal policy |

| Earthquake insurance (CEA) | Seismic damage to structure and systems | Flood, fire following quake (covered by homeowners) | Separate state policy |

How to file an HVAC insurance claim in California

Filing a successful HVAC claim requires preparation before you call your insurer. Documenting HVAC damage thoroughly with photos and getting multiple contractor bids before cleanup gives your claim the strongest possible foundation. Adjusters work from evidence. The more specific and dated your documentation, the harder it is to deny.

Follow these steps in order:

- Photograph and video everything before touching the damaged equipment. Capture the damage from multiple angles, including any external cause such as a fallen branch or scorch marks.

- Call your insurer to open a claim as soon as possible. Most policies require prompt notification after a loss.

- Get a written assessment from a licensed HVAC contractor that explicitly links the damage to the covered event. Vague reports that simply say "unit not working" are not enough.

- Obtain at least three contractor bids for repair or replacement. Adjusters often use the lowest reasonable bid as their baseline.

- Review your policy's ACV vs. RCV terms before accepting any settlement offer. If your policy is RCV, make sure the adjuster is not calculating depreciation.

- Submit all documentation together: photos, contractor assessment, bids, and any prior maintenance records.

- Follow up in writing after every conversation with your adjuster. Email creates a paper trail that phone calls do not.

Pro Tip: A licensed HVAC professional's written assessment that ties the damage directly to a covered event is often the single most important document in your claim file. Do not skip this step.

For guidance on the broader claim documentation process, filing storm damage claims follows the same evidence-based logic that applies to HVAC claims.

How California's unique risks affect your HVAC coverage

California homeowners face regional risks that directly affect HVAC coverage decisions. Wildfires can destroy outdoor condenser units and fill indoor air handlers with smoke and ash. Santa Ana windstorms regularly knock over exterior equipment. Neither earthquake nor flood damage is covered under a standard homeowners policy, and both are real threats in California.

Wildfire smoke damage to HVAC systems sits in a gray area. If fire physically damages the unit, Coverage A applies. If smoke infiltrates the ductwork and the system itself is intact, coverage depends on your specific policy language. Some insurers cover smoke damage as a named peril. Others do not. Reading your policy's smoke damage clause before wildfire season is worth the 20 minutes it takes.

The California insurance market has tightened significantly in recent years. Several major carriers have reduced their exposure in high-risk fire zones, which means some homeowners are now on the California FAIR Plan, a state-backed insurer of last resort. FAIR Plan policies are more limited than standard homeowners policies, and HVAC coverage under those plans deserves a direct conversation with your agent.

Consulting a local independent insurance agent who specializes in California properties is the most reliable way to identify gaps in your current coverage. Reviewing your policy annually, especially after a major weather event or after installing new HVAC equipment, keeps your coverage aligned with your actual exposure. For maintenance practices that reduce your claim risk, proven ways to extend HVAC lifespan covers the practical steps California homeowners should follow year-round.

Key takeaways

Home insurance covers HVAC systems only for sudden, accidental damage from named perils. Wear and tear, mechanical failure, and deferred maintenance are excluded without additional endorsements.

| Point | Details |

|---|---|

| Standard coverage is event-based | Fire, lightning, windstorms, and burst pipes trigger coverage; aging and breakdowns do not. |

| Equipment Breakdown fills the gap | Add this endorsement to cover compressor failures and electrical burnouts excluded by standard policies. |

| ACV vs. RCV changes your payout | RCV policies pay full replacement cost; ACV policies deduct depreciation, often cutting settlements significantly. |

| Documentation wins claims | Photos, a licensed contractor's written assessment, and maintenance records are the three pillars of a successful claim. |

| California needs extra policies | Earthquake and flood damage require separate coverage; wildfire smoke damage depends on specific policy language. |

What I've learned after years of HVAC work in California

The homeowners who get their claims paid are almost always the ones who treated their HVAC system like an asset worth protecting, not just a machine to ignore until it breaks. I have seen adjusters deny claims on systems that were genuinely storm-damaged, simply because the maintenance history was nonexistent and the unit showed obvious signs of neglect. The insurer did not have to prove the storm did not cause the damage. They just had to show the system was already compromised.

My honest advice: pull out your homeowners policy today and find three things. First, confirm whether it is ACV or RCV. Second, check whether Equipment Breakdown coverage is listed as an endorsement. Third, read the smoke damage clause. Most homeowners in California have never done this, and they find out what their policy actually says at the worst possible moment.

Regular maintenance is not just about keeping your system running. It is your best defense against a claim denial. A clean, well-documented system is much harder for an adjuster to dismiss. If you are unsure what your HVAC system needs, common HVAC maintenance myths are worth reading before you assume you are covered for something you are not.

— Edward

Get expert HVAC support from E320air

When your HVAC system is damaged and you need documentation that holds up to insurer scrutiny, the quality of your contractor's assessment matters. E320air serves California homeowners with HVAC repairs, maintenance, and full system installations. The team provides written assessments that clearly connect damage to its cause, which is exactly what adjusters need to approve a claim.

Whether you need an emergency repair after a storm, a pre-claim inspection to document your system's condition, or a full HVAC installation after a total loss, E320air has the licensed expertise to help. Visit E320air to schedule a service call or request an assessment for your insurance claim.

FAQ

Does home insurance cover HVAC replacement?

Home insurance covers HVAC replacement only when the system is destroyed by a covered peril such as fire, lightning, or a windstorm. Replacement due to age, mechanical failure, or wear and tear is not covered under a standard policy.

What is Equipment Breakdown coverage for HVAC?

Equipment Breakdown coverage is an endorsement added to a homeowners policy that covers mechanical and electrical failures of HVAC systems, including compressor failures and control board burnouts, which standard policies exclude.

Does homeowners insurance cover HVAC in California earthquakes?

No. Earthquake damage requires a separate earthquake insurance policy, such as one through the California Earthquake Authority. Standard homeowners insurance does not cover seismic damage to any part of your home, including HVAC systems.

How do I get my insurance to pay for HVAC damage?

Document the damage with photos before any cleanup, obtain a written assessment from a licensed HVAC contractor linking the damage to a covered event, and submit at least three contractor bids with your claim. A clear paper trail connecting the damage to a named peril is the most reliable path to claim approval.

Is HVAC wear and tear ever covered by home insurance?

No. Wear and tear, gradual deterioration, and mechanical breakdowns from normal use are excluded from standard homeowners insurance. Equipment Breakdown endorsements or a home warranty are the appropriate products for those types of failures.